# Import packages

import numpy as np

import pandas as pd

import seaborn as snsLecture 2 - Introduction to Pandas

Overview

This lecture provides an introduction to Pandas, a Python package with structures and data manipulation tools designed to make data cleaning and analysis fast and convenient. Topics include:

- Pandas objects (

pd.Series,pd.DataFrame) - Essential pandas functionality (indexing, selection, filtering, operations on dataframes)

- The concept of tidy data (Wickham, 2014)

References

This lecture contains material from:

- Chapter 5, Python for Data Analysis, 3E (Wes McKinney, 2022)

- Pierre Bellec’s notes

About Pandas

Pandas is the Python module that provides functionality similar to R’s built-in data.frame object. Pandas is designed for working with tabular or heterogeneous data.

Pandas Series

A Series is a one-dimensional array-like object containing a sequence of values (of similar types to NumPy types) of the same type and an associated array of data labels, called its index.

s = pd.Series([2, 4, -1, 5])

s0 2

1 4

2 -1

3 5

dtype: int64s.array<NumpyExtensionArray>

[np.int64(2), np.int64(4), np.int64(-1), np.int64(5)]

Length: 4, dtype: int64s.indexRangeIndex(start=0, stop=4, step=1)s = pd.Series([2, 4, -1, 5], index=['a', 'b', 'c', 'd'])s.indexIndex(['a', 'b', 'c', 'd'], dtype='object')s['a']np.int64(2)s[['a', 'd']]a 2

d 5

dtype: int64s * 2a 4

b 8

c -2

d 10

dtype: int64s[s>2]b 4

d 5

dtype: int64We can create a series from a numpy array:

# Creating a numpy array

a = np.arange(6, 15, 1) + 0.2

print(a.shape)

a(9,)array([ 6.2, 7.2, 8.2, 9.2, 10.2, 11.2, 12.2, 13.2, 14.2])s_from_np = pd.Series(a)

s_from_np0 6.2

1 7.2

2 8.2

3 9.2

4 10.2

5 11.2

6 12.2

7 13.2

8 14.2

dtype: float64s_from_np.array<NumpyExtensionArray>

[ np.float64(6.2), np.float64(7.2), np.float64(8.2), np.float64(9.2),

np.float64(10.2), np.float64(11.2), np.float64(12.2), np.float64(13.2),

np.float64(14.2)]

Length: 9, dtype: float64s_from_np.indexRangeIndex(start=0, stop=9, step=1)We can adjust the index in place:

s_from_np.index = [2 * i for i in range(len(s_from_np))]s_from_np0 6.2

2 7.2

4 8.2

6 9.2

8 10.2

10 11.2

12 12.2

14 13.2

16 14.2

dtype: float64Finally, we can turn the Series object back to an ndarray as:

s_from_np.to_numpy()array([ 6.2, 7.2, 8.2, 9.2, 10.2, 11.2, 12.2, 13.2, 14.2])We can also create a series from a dictionary:

dat = {"Ohio": 35000, "Texas": 71000, "Oregon": 16000, "Utah": 5000}

s_from_dict = pd.Series(dat)

s_from_dictOhio 35000

Texas 71000

Oregon 16000

Utah 5000

dtype: int64s_from_dict.to_dict(){'Ohio': 35000, 'Texas': 71000, 'Oregon': 16000, 'Utah': 5000}states = ["California", "Ohio", "Oregon", "Texas"]s_new = pd.Series(dat, index=states)s_newCalifornia NaN

Ohio 35000.0

Oregon 16000.0

Texas 71000.0

dtype: float64pd.isna(s_new)California True

Ohio False

Oregon False

Texas False

dtype: boolpd.notna(s_new)California False

Ohio True

Oregon True

Texas True

dtype: bools_new.isna()California True

Ohio False

Oregon False

Texas False

dtype: boolPandas DataFrame

A DataFrame represents a rectangular table of data and contains an ordered, named collection of columns, each of which can be a different value type (numeric, string, Boolean, etc.). The DataFrame has both a row and column index; it can be thought of as a dictionary of Series all sharing the same index.

data = {"state": ["Ohio", "Ohio", "Ohio", "Nevada", "Nevada", "Nevada"],

"year": [2000, 2001, 2002, 2001, 2002, 2003],

"pop": [1.5, 1.7, 3.6, 2.4, 2.9, 3.2]}

frame = pd.DataFrame(data)frame| state | year | pop | |

|---|---|---|---|

| 0 | Ohio | 2000 | 1.5 |

| 1 | Ohio | 2001 | 1.7 |

| 2 | Ohio | 2002 | 3.6 |

| 3 | Nevada | 2001 | 2.4 |

| 4 | Nevada | 2002 | 2.9 |

| 5 | Nevada | 2003 | 3.2 |

# adding a column (similar to dictionaries)

frame['debt'] = 16frame| state | year | pop | debt | |

|---|---|---|---|---|

| 0 | Ohio | 2000 | 1.5 | 16 |

| 1 | Ohio | 2001 | 1.7 | 16 |

| 2 | Ohio | 2002 | 3.6 | 16 |

| 3 | Nevada | 2001 | 2.4 | 16 |

| 4 | Nevada | 2002 | 2.9 | 16 |

| 5 | Nevada | 2003 | 3.2 | 16 |

len(frame)6frame['debt'] = np.linspace(16,20,num=len(frame))

frame| state | year | pop | debt | |

|---|---|---|---|---|

| 0 | Ohio | 2000 | 1.5 | 16.0 |

| 1 | Ohio | 2001 | 1.7 | 16.8 |

| 2 | Ohio | 2002 | 3.6 | 17.6 |

| 3 | Nevada | 2001 | 2.4 | 18.4 |

| 4 | Nevada | 2002 | 2.9 | 19.2 |

| 5 | Nevada | 2003 | 3.2 | 20.0 |

# another example

A2d = np.random.normal(size=(8, 2))

A2d.shape(8, 2)df_from_np = pd.DataFrame(A2d)

df_from_np| 0 | 1 | |

|---|---|---|

| 0 | -2.372890 | 0.461543 |

| 1 | -0.280463 | 1.104957 |

| 2 | -0.078033 | -0.759848 |

| 3 | 1.013987 | 0.562257 |

| 4 | 0.168685 | 0.785529 |

| 5 | -0.862294 | -0.784686 |

| 6 | -1.642501 | -0.204560 |

| 7 | 0.056823 | 0.733871 |

df_from_np.head()| 0 | 1 | |

|---|---|---|

| 0 | -2.372890 | 0.461543 |

| 1 | -0.280463 | 1.104957 |

| 2 | -0.078033 | -0.759848 |

| 3 | 1.013987 | 0.562257 |

| 4 | 0.168685 | 0.785529 |

df_from_np.tail()| 0 | 1 | |

|---|---|---|

| 3 | 1.013987 | 0.562257 |

| 4 | 0.168685 | 0.785529 |

| 5 | -0.862294 | -0.784686 |

| 6 | -1.642501 | -0.204560 |

| 7 | 0.056823 | 0.733871 |

df_from_np.to_numpy()array([[-2.37288997, 0.4615429 ],

[-0.28046288, 1.10495676],

[-0.07803338, -0.75984847],

[ 1.01398664, 0.5622572 ],

[ 0.16868548, 0.78552939],

[-0.86229404, -0.78468577],

[-1.64250143, -0.20455967],

[ 0.05682344, 0.73387118]])Indices

df_from_np.indexRangeIndex(start=0, stop=8, step=1)indices = list('abcdefgh')

indices['a', 'b', 'c', 'd', 'e', 'f', 'g', 'h']df_from_np = pd.DataFrame(A2d, index=indices)

df_from_np| 0 | 1 | |

|---|---|---|

| a | -2.372890 | 0.461543 |

| b | -0.280463 | 1.104957 |

| c | -0.078033 | -0.759848 |

| d | 1.013987 | 0.562257 |

| e | 0.168685 | 0.785529 |

| f | -0.862294 | -0.784686 |

| g | -1.642501 | -0.204560 |

| h | 0.056823 | 0.733871 |

isinstance(df_from_np.index, pd.Series)Falseisinstance(df_from_np.columns, pd.Index)Trueobj = pd.Series([4.5, 7.2,-5.3, 3.6], index=["d", "b", "a", "c"])obj.reindex(['a', 'b', 'c', 'd', 'e'])a -5.3

b 7.2

c 3.6

d 4.5

e NaN

dtype: float64obj2 = obj.reindex(['a', 'a', 'b', 'c', 'd'])obj2.index.is_uniqueFalseobj2.index.unique()Index(['a', 'b', 'c', 'd'], dtype='object')obj2['a']a -5.3

a -5.3

dtype: float64obj2.index.isin(['a'])array([ True, True, False, False, False])Columns

df_from_np.columnsRangeIndex(start=0, stop=2, step=1)df_from_np.columns = ['firstCol', 'secondCol']

df_from_np| firstCol | secondCol | |

|---|---|---|

| a | -2.372890 | 0.461543 |

| b | -0.280463 | 1.104957 |

| c | -0.078033 | -0.759848 |

| d | 1.013987 | 0.562257 |

| e | 0.168685 | 0.785529 |

| f | -0.862294 | -0.784686 |

| g | -1.642501 | -0.204560 |

| h | 0.056823 | 0.733871 |

isinstance(df_from_np.columns, pd.Series)Falseisinstance(df_from_np.columns, pd.Index)TrueDatatypes

df_from_np.dtypesfirstCol float64

secondCol float64

dtype: objectdf = pd.DataFrame([['a', 1, 'b'], [1, 2, 3]])df| 0 | 1 | 2 | |

|---|---|---|---|

| 0 | a | 1 | b |

| 1 | 1 | 2 | 3 |

df.dtypes0 object

1 int64

2 object

dtype: objecttype(df.dtypes)pandas.core.series.Seriesisinstance(df.dtypes, pd.Series)TrueIllustration: Historical Rates Data

Reading in csv files

First, make sure the file is in your working directory - this is ‘where you are currently’ on the computer.

Python needs to know where the files live - they can be on your computer (local) or on the internet (remote).

The place where your file lives is referred to as its ‘path’. You can think of the path as directions to the file. There are two kinds of paths:

- relative paths indicate where a file is with respect to your working directory

- absolute paths indicate where the file is with respect to the computers filesystem base (or root) folder, regardless of where you are working

Image from Data Science: A first introduction with Python (link)

In VSCode, your working directory is typically where your Jupyter notebook is saved.

import os

os.getcwd()'/Users/gm845/Library/CloudStorage/Box-Box/teaching/2025/msds-597/website/lec-2'We will be working with exchange rates data from the European Central Bank.

This data has the path:

/Users/gm845/Library/CloudStorage/Box-Box/teaching/2025/msds-597/lectures/data/rates.csvTo get to rates.csv, I need to “go one level up”, then enter the “data” folder.

Relative to the Jupyter notebook, this path is ../data/rates.csv. Here, ../ indicates “go one level up”.

df = pd.read_csv('../data/rates.csv')Note: the default is header=0 which takes the first row in the csv file as the column names.

Let’s look at the dataframe.

df.head() | Time | USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2024-04-16 | 1.0637 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 |

| 1 | 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 |

| 2 | 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 |

| 3 | 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 |

| 4 | 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 |

df.tail()| Time | USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|---|

| 57 | 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 |

| 58 | 2024-01-23 | 1.0872 | 160.88 | 1.9558 | 24.824 | 7.4574 | 0.85493 | 0.9446 |

| 59 | 2024-01-22 | 1.0890 | 160.95 | 1.9558 | 24.758 | 7.4585 | 0.85575 | 0.9458 |

| 60 | 2024-01-19 | 1.0887 | 161.17 | 1.9558 | 24.813 | 7.4575 | 0.85825 | 0.9459 |

| 61 | 2024-01-18 | 1.0875 | 160.89 | 1.9558 | 24.734 | 7.4571 | 0.85773 | 0.9432 |

df.shape(62, 8)We can inspect the data types of each column:

df.dtypesTime object

USD float64

JPY float64

BGN float64

CZK float64

DKK float64

GBP float64

CHF float64

dtype: objectWe see that the Time column has type object. We can fix this by reading in the data again, this time with the argument parse_dates=[`Time`]

df = pd.read_csv('../data/rates.csv', parse_dates=['Time'])

df.dtypesTime datetime64[ns]

USD float64

JPY float64

BGN float64

CZK float64

DKK float64

GBP float64

CHF float64

dtype: objectAccessing a column

df['USD']0 1.0637

1 1.0656

2 1.0652

3 1.0729

4 1.0860

...

57 1.0905

58 1.0872

59 1.0890

60 1.0887

61 1.0875

Name: USD, Length: 62, dtype: float64isinstance(df['USD'], pd.Series)Truedf.USD0 1.0637

1 1.0656

2 1.0652

3 1.0729

4 1.0860

...

57 1.0905

58 1.0872

59 1.0890

60 1.0887

61 1.0875

Name: USD, Length: 62, dtype: float64Note: when we get the USD rates, we unfortunately lose information about the time.

# here is how to fix it and use time is index

df.index = df['Time']

df| Time | USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|---|

| Time | ||||||||

| 2024-04-16 | 2024-04-16 | 1.0637 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 |

| 2024-04-15 | 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 |

| 2024-04-12 | 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 |

| 2024-04-11 | 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 |

| 2024-04-10 | 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 |

| 2024-01-23 | 2024-01-23 | 1.0872 | 160.88 | 1.9558 | 24.824 | 7.4574 | 0.85493 | 0.9446 |

| 2024-01-22 | 2024-01-22 | 1.0890 | 160.95 | 1.9558 | 24.758 | 7.4585 | 0.85575 | 0.9458 |

| 2024-01-19 | 2024-01-19 | 1.0887 | 161.17 | 1.9558 | 24.813 | 7.4575 | 0.85825 | 0.9459 |

| 2024-01-18 | 2024-01-18 | 1.0875 | 160.89 | 1.9558 | 24.734 | 7.4571 | 0.85773 | 0.9432 |

62 rows × 8 columns

# Now when we extract a column, we keep the index

# we keep information about the dates

df.USDTime

2024-04-16 1.0637

2024-04-15 1.0656

2024-04-12 1.0652

2024-04-11 1.0729

2024-04-10 1.0860

...

2024-01-24 1.0905

2024-01-23 1.0872

2024-01-22 1.0890

2024-01-19 1.0887

2024-01-18 1.0875

Name: USD, Length: 62, dtype: float64Selecting/dropping multiple columns or rows

# Subsets of columns

df[['USD', 'CHF']]| USD | CHF | |

|---|---|---|

| Time | ||

| 2024-04-16 | 1.0637 | 0.9712 |

| 2024-04-15 | 1.0656 | 0.9725 |

| 2024-04-12 | 1.0652 | 0.9716 |

| 2024-04-11 | 1.0729 | 0.9787 |

| 2024-04-10 | 1.0860 | 0.9810 |

| ... | ... | ... |

| 2024-01-24 | 1.0905 | 0.9415 |

| 2024-01-23 | 1.0872 | 0.9446 |

| 2024-01-22 | 1.0890 | 0.9458 |

| 2024-01-19 | 1.0887 | 0.9459 |

| 2024-01-18 | 1.0875 | 0.9432 |

62 rows × 2 columns

df[['USD', 'CHF']].head()| USD | CHF | |

|---|---|---|

| Time | ||

| 2024-04-16 | 1.0637 | 0.9712 |

| 2024-04-15 | 1.0656 | 0.9725 |

| 2024-04-12 | 1.0652 | 0.9716 |

| 2024-04-11 | 1.0729 | 0.9787 |

| 2024-04-10 | 1.0860 | 0.9810 |

df

df_dropped = df.drop(columns=['Time', 'BGN', 'DKK', 'CZK'])

df_dropped.head()| USD | JPY | GBP | CHF | |

|---|---|---|---|---|

| Time | ||||

| 2024-04-16 | 1.0637 | 164.54 | 0.85440 | 0.9712 |

| 2024-04-15 | 1.0656 | 164.05 | 0.85405 | 0.9725 |

| 2024-04-12 | 1.0652 | 163.16 | 0.85424 | 0.9716 |

| 2024-04-11 | 1.0729 | 164.18 | 0.85525 | 0.9787 |

| 2024-04-10 | 1.0860 | 164.89 | 0.85515 | 0.9810 |

df.head() # original df unaffected| Time | USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|---|

| Time | ||||||||

| 2024-04-16 | 2024-04-16 | 1.0637 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 |

| 2024-04-15 | 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 |

| 2024-04-12 | 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 |

| 2024-04-11 | 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 |

| 2024-04-10 | 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 |

# dropping a row

df_dropped.drop('2024-04-16').head()

# same as: df_dropped.drop(index='2024-04-16').head()| USD | JPY | GBP | CHF | |

|---|---|---|---|---|

| Time | ||||

| 2024-04-15 | 1.0656 | 164.05 | 0.85405 | 0.9725 |

| 2024-04-12 | 1.0652 | 163.16 | 0.85424 | 0.9716 |

| 2024-04-11 | 1.0729 | 164.18 | 0.85525 | 0.9787 |

| 2024-04-10 | 1.0860 | 164.89 | 0.85515 | 0.9810 |

| 2024-04-09 | 1.0867 | 164.97 | 0.85663 | 0.9819 |

# now that time is the index, let's drop the Time column

df = df.drop(columns='Time')Selecting rows

Series

Note: be careful with accessing data - it will treat integers as labels

usd = df['USD'].copy()usd.index = [i * 2 for i in range(len(usd))]usd0 1.0637

2 1.0656

4 1.0652

6 1.0729

8 1.0860

...

114 1.0905

116 1.0872

118 1.0890

120 1.0887

122 1.0875

Name: USD, Length: 62, dtype: float64usd[2]np.float64(1.0656)To avoid this, use the .loc method for labels, and .iloc for integers.

usd.loc[2]np.float64(1.0656)usd.iloc[2]np.float64(1.0652)Dataframes

df.loc['2024-04-16']USD 1.0637

JPY 164.5400

BGN 1.9558

CZK 25.2100

DKK 7.4609

GBP 0.8544

CHF 0.9712

Name: 2024-04-16 00:00:00, dtype: float64df.loc['2024-04-16', ['USD', 'GBP']]USD 1.0637

GBP 0.8544

Name: 2024-04-16 00:00:00, dtype: float64df.loc[["2024-01-18"], ['USD', 'GBP']]| USD | GBP | |

|---|---|---|

| Time | ||

| 2024-01-18 | 1.0875 | 0.85773 |

print('First is', type(df.loc["2024-01-18", ['USD', 'GBP']]), ', second is', type(df.loc[["2024-01-18"], ['USD', 'GBP']]))First is <class 'pandas.core.series.Series'> , second is <class 'pandas.core.frame.DataFrame'>df.loc[["2024-01-18", "2024-04-16"], ['USD', 'GBP']]| USD | GBP | |

|---|---|---|

| Time | ||

| 2024-01-18 | 1.0875 | 0.85773 |

| 2024-04-16 | 1.0637 | 0.85440 |

# this will fail: df.loc[:, 1:3]

# loc expects labels for rows and columnsiloc

df.iloc[0]USD 1.0637

JPY 164.5400

BGN 1.9558

CZK 25.2100

DKK 7.4609

GBP 0.8544

CHF 0.9712

Name: 2024-04-16 00:00:00, dtype: float64df.iloc[:, 1:3]| JPY | BGN | |

|---|---|---|

| Time | ||

| 2024-04-16 | 164.54 | 1.9558 |

| 2024-04-15 | 164.05 | 1.9558 |

| 2024-04-12 | 163.16 | 1.9558 |

| 2024-04-11 | 164.18 | 1.9558 |

| 2024-04-10 | 164.89 | 1.9558 |

| ... | ... | ... |

| 2024-01-24 | 160.46 | 1.9558 |

| 2024-01-23 | 160.88 | 1.9558 |

| 2024-01-22 | 160.95 | 1.9558 |

| 2024-01-19 | 161.17 | 1.9558 |

| 2024-01-18 | 160.89 | 1.9558 |

62 rows × 2 columns

df.iloc[:, 1:] # all columns except 0th one| JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|

| Time | ||||||

| 2024-04-16 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 |

| 2024-04-15 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 |

| 2024-04-12 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 |

| 2024-04-11 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 |

| 2024-04-10 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 |

| ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 |

| 2024-01-23 | 160.88 | 1.9558 | 24.824 | 7.4574 | 0.85493 | 0.9446 |

| 2024-01-22 | 160.95 | 1.9558 | 24.758 | 7.4585 | 0.85575 | 0.9458 |

| 2024-01-19 | 161.17 | 1.9558 | 24.813 | 7.4575 | 0.85825 | 0.9459 |

| 2024-01-18 | 160.89 | 1.9558 | 24.734 | 7.4571 | 0.85773 | 0.9432 |

62 rows × 6 columns

df.iloc[:10, 1:4] # select a few rows, only keep columns 1,2,3| JPY | BGN | CZK | |

|---|---|---|---|

| Time | |||

| 2024-04-16 | 164.54 | 1.9558 | 25.210 |

| 2024-04-15 | 164.05 | 1.9558 | 25.324 |

| 2024-04-12 | 163.16 | 1.9558 | 25.337 |

| 2024-04-11 | 164.18 | 1.9558 | 25.392 |

| 2024-04-10 | 164.89 | 1.9558 | 25.368 |

| 2024-04-09 | 164.97 | 1.9558 | 25.380 |

| 2024-04-08 | 164.43 | 1.9558 | 25.354 |

| 2024-04-05 | 164.10 | 1.9558 | 25.286 |

| 2024-04-04 | 164.69 | 1.9558 | 25.322 |

| 2024-04-03 | 163.66 | 1.9558 | 25.352 |

| Type | Notes |

|---|---|

df[column] |

Select single column or sequence of columns from the DataFrame; special case conveniences: Boolean array (filter rows), slice (slice rows), or Boolean DataFrame (set values based on some criterion) |

df.loc[rows] |

Select single row or subset of rows from the DataFrame by label |

df.loc[:,cols] |

Select single column or subset of columns by label |

df.loc[rows,cols] |

Select both row(s) and column(s) by label |

df.iloc[rows] |

Select single row or subset of rows from the DataFrame by integer position |

df.iloc[:,cols] |

Select single column or subset of columns by integer position |

df.iloc[rows,cols] |

Select both row(s) and column(s) by integer position |

Selecting based on logical conditions

df.query('USD > 1.09')| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-03-21 | 1.0907 | 164.96 | 1.9558 | 25.243 | 7.4579 | 0.85678 | 0.9766 |

| 2024-03-14 | 1.0925 | 161.70 | 1.9558 | 25.198 | 7.4568 | 0.85420 | 0.9616 |

| 2024-03-13 | 1.0939 | 161.83 | 1.9558 | 25.273 | 7.4573 | 0.85451 | 0.9599 |

| 2024-03-12 | 1.0916 | 161.39 | 1.9558 | 25.272 | 7.4571 | 0.85458 | 0.9588 |

| 2024-03-11 | 1.0926 | 160.43 | 1.9558 | 25.322 | 7.4552 | 0.85208 | 0.9594 |

| 2024-03-08 | 1.0932 | 160.99 | 1.9558 | 25.308 | 7.4547 | 0.85168 | 0.9588 |

| 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 |

df.query('USD > 1.09 and JPY < 161')| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-03-11 | 1.0926 | 160.43 | 1.9558 | 25.322 | 7.4552 | 0.85208 | 0.9594 |

| 2024-03-08 | 1.0932 | 160.99 | 1.9558 | 25.308 | 7.4547 | 0.85168 | 0.9588 |

| 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 |

df.USD > 1.09 # boolean maskTime

2024-04-16 False

2024-04-15 False

2024-04-12 False

2024-04-11 False

2024-04-10 False

...

2024-01-24 True

2024-01-23 False

2024-01-22 False

2024-01-19 False

2024-01-18 False

Name: USD, Length: 62, dtype: booldf[df.USD > 1.09] # you can select boolean rows with []| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-03-21 | 1.0907 | 164.96 | 1.9558 | 25.243 | 7.4579 | 0.85678 | 0.9766 |

| 2024-03-14 | 1.0925 | 161.70 | 1.9558 | 25.198 | 7.4568 | 0.85420 | 0.9616 |

| 2024-03-13 | 1.0939 | 161.83 | 1.9558 | 25.273 | 7.4573 | 0.85451 | 0.9599 |

| 2024-03-12 | 1.0916 | 161.39 | 1.9558 | 25.272 | 7.4571 | 0.85458 | 0.9588 |

| 2024-03-11 | 1.0926 | 160.43 | 1.9558 | 25.322 | 7.4552 | 0.85208 | 0.9594 |

| 2024-03-08 | 1.0932 | 160.99 | 1.9558 | 25.308 | 7.4547 | 0.85168 | 0.9588 |

| 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 |

mask1 = df.USD > 1.09

mask2 = df.JPY < 161df[mask1 & mask2] # mask1 and mask2| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-03-11 | 1.0926 | 160.43 | 1.9558 | 25.322 | 7.4552 | 0.85208 | 0.9594 |

| 2024-03-08 | 1.0932 | 160.99 | 1.9558 | 25.308 | 7.4547 | 0.85168 | 0.9588 |

| 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 |

df[mask1 | mask2].head() # mask1 or mask2| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-03-21 | 1.0907 | 164.96 | 1.9558 | 25.243 | 7.4579 | 0.85678 | 0.9766 |

| 2024-03-14 | 1.0925 | 161.70 | 1.9558 | 25.198 | 7.4568 | 0.85420 | 0.9616 |

| 2024-03-13 | 1.0939 | 161.83 | 1.9558 | 25.273 | 7.4573 | 0.85451 | 0.9599 |

| 2024-03-12 | 1.0916 | 161.39 | 1.9558 | 25.272 | 7.4571 | 0.85458 | 0.9588 |

| 2024-03-11 | 1.0926 | 160.43 | 1.9558 | 25.322 | 7.4552 | 0.85208 | 0.9594 |

# this fails

# df[mask1 & mask2, 'USD']

# to select rows with booleans AND columns, use locBoolean arrays can be used with loc but not iloc:

df.loc[mask1 & mask2, 'USD']Time

2024-03-11 1.0926

2024-03-08 1.0932

2024-01-24 1.0905

Name: USD, dtype: float64# Using a boolean mask to select columns

df.columns != 'Time'array([ True, True, True, True, True, True, True])df_dropped2 = df.loc[:, df.columns != 'Time']

df_dropped2| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | 1.0637 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 |

| 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 |

| 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 |

| 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 |

| 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 |

| 2024-01-23 | 1.0872 | 160.88 | 1.9558 | 24.824 | 7.4574 | 0.85493 | 0.9446 |

| 2024-01-22 | 1.0890 | 160.95 | 1.9558 | 24.758 | 7.4585 | 0.85575 | 0.9458 |

| 2024-01-19 | 1.0887 | 161.17 | 1.9558 | 24.813 | 7.4575 | 0.85825 | 0.9459 |

| 2024-01-18 | 1.0875 | 160.89 | 1.9558 | 24.734 | 7.4571 | 0.85773 | 0.9432 |

62 rows × 7 columns

Sorting dataframes

df.sort_index()| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-01-18 | 1.0875 | 160.89 | 1.9558 | 24.734 | 7.4571 | 0.85773 | 0.9432 |

| 2024-01-19 | 1.0887 | 161.17 | 1.9558 | 24.813 | 7.4575 | 0.85825 | 0.9459 |

| 2024-01-22 | 1.0890 | 160.95 | 1.9558 | 24.758 | 7.4585 | 0.85575 | 0.9458 |

| 2024-01-23 | 1.0872 | 160.88 | 1.9558 | 24.824 | 7.4574 | 0.85493 | 0.9446 |

| 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 |

| 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 |

| 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 |

| 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 |

| 2024-04-16 | 1.0637 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 |

62 rows × 7 columns

df.sort_index(axis='columns')| BGN | CHF | CZK | DKK | GBP | JPY | USD | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | 1.9558 | 0.9712 | 25.210 | 7.4609 | 0.85440 | 164.54 | 1.0637 |

| 2024-04-15 | 1.9558 | 0.9725 | 25.324 | 7.4606 | 0.85405 | 164.05 | 1.0656 |

| 2024-04-12 | 1.9558 | 0.9716 | 25.337 | 7.4603 | 0.85424 | 163.16 | 1.0652 |

| 2024-04-11 | 1.9558 | 0.9787 | 25.392 | 7.4604 | 0.85525 | 164.18 | 1.0729 |

| 2024-04-10 | 1.9558 | 0.9810 | 25.368 | 7.4594 | 0.85515 | 164.89 | 1.0860 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 1.9558 | 0.9415 | 24.786 | 7.4568 | 0.85543 | 160.46 | 1.0905 |

| 2024-01-23 | 1.9558 | 0.9446 | 24.824 | 7.4574 | 0.85493 | 160.88 | 1.0872 |

| 2024-01-22 | 1.9558 | 0.9458 | 24.758 | 7.4585 | 0.85575 | 160.95 | 1.0890 |

| 2024-01-19 | 1.9558 | 0.9459 | 24.813 | 7.4575 | 0.85825 | 161.17 | 1.0887 |

| 2024-01-18 | 1.9558 | 0.9432 | 24.734 | 7.4571 | 0.85773 | 160.89 | 1.0875 |

62 rows × 7 columns

df.USD.sort_values(ascending=False)Time

2024-03-13 1.0939

2024-03-08 1.0932

2024-03-11 1.0926

2024-03-14 1.0925

2024-03-12 1.0916

...

2024-04-11 1.0729

2024-02-14 1.0713

2024-04-15 1.0656

2024-04-12 1.0652

2024-04-16 1.0637

Name: USD, Length: 62, dtype: float64df_sorted = df.sort_values(by='USD', ascending=False)df_sorted.head()| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-03-13 | 1.0939 | 161.83 | 1.9558 | 25.273 | 7.4573 | 0.85451 | 0.9599 |

| 2024-03-08 | 1.0932 | 160.99 | 1.9558 | 25.308 | 7.4547 | 0.85168 | 0.9588 |

| 2024-03-11 | 1.0926 | 160.43 | 1.9558 | 25.322 | 7.4552 | 0.85208 | 0.9594 |

| 2024-03-14 | 1.0925 | 161.70 | 1.9558 | 25.198 | 7.4568 | 0.85420 | 0.9616 |

| 2024-03-12 | 1.0916 | 161.39 | 1.9558 | 25.272 | 7.4571 | 0.85458 | 0.9588 |

Unique values

df.USD.unique()array([1.0637, 1.0656, 1.0652, 1.0729, 1.086 , 1.0867, 1.0823, 1.0841,

1.0852, 1.0783, 1.0749, 1.0811, 1.0816, 1.0855, 1.0835, 1.0907,

1.0844, 1.0854, 1.0892, 1.0925, 1.0939, 1.0916, 1.0926, 1.0932,

1.0895, 1.0874, 1.0849, 1.0846, 1.0813, 1.0826, 1.0808, 1.0856,

1.0834, 1.0809, 1.0802, 1.0776, 1.0768, 1.0743, 1.0713, 1.0793,

1.0773, 1.0772, 1.0758, 1.0746, 1.0883, 1.0814, 1.0837, 1.0871,

1.0893, 1.0905, 1.0872, 1.089 , 1.0887, 1.0875])df.USD.value_counts().head()USD

1.0823 3

1.0846 2

1.0844 2

1.0776 2

1.0852 2

Name: count, dtype: int64df.BGN.unique()array([1.9558])df.BGN.value_counts()BGN

1.9558 62

Name: count, dtype: int64Adding or modifying columns

df_copy = df.copy() # copy by value, not by referencedf_copy['new_col'] = 100 * df_copy.JPY/df_copy.USDdf_copy.head()| USD | JPY | BGN | CZK | DKK | GBP | CHF | new_col | |

|---|---|---|---|---|---|---|---|---|

| Time | ||||||||

| 2024-04-16 | 1.0637 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 | 15468.647175 |

| 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 | 15395.082583 |

| 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 | 15317.311303 |

| 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 | 15302.451300 |

| 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 | 15183.241252 |

df_copy[df_copy > 200] = 200# if we are changing a single column, use loc

df_copy.loc[df_copy['new_col'] == 200, 'new_col'] = 0df_copy| USD | JPY | BGN | CZK | DKK | GBP | CHF | new_col | |

|---|---|---|---|---|---|---|---|---|

| Time | ||||||||

| 2024-04-16 | 1.0637 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 | 0.0 |

| 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 | 0.0 |

| 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 | 0.0 |

| 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 | 0.0 |

| 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 | 0.0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 | 0.0 |

| 2024-01-23 | 1.0872 | 160.88 | 1.9558 | 24.824 | 7.4574 | 0.85493 | 0.9446 | 0.0 |

| 2024-01-22 | 1.0890 | 160.95 | 1.9558 | 24.758 | 7.4585 | 0.85575 | 0.9458 | 0.0 |

| 2024-01-19 | 1.0887 | 161.17 | 1.9558 | 24.813 | 7.4575 | 0.85825 | 0.9459 | 0.0 |

| 2024-01-18 | 1.0875 | 160.89 | 1.9558 | 24.734 | 7.4571 | 0.85773 | 0.9432 | 0.0 |

62 rows × 8 columns

Alternatively, we can use the assign function to create a new dataframe with the new column:

df.assign(new = df.USD/df.JPY * 100)| USD | JPY | BGN | CZK | DKK | GBP | CHF | new | |

|---|---|---|---|---|---|---|---|---|

| Time | ||||||||

| 2024-04-16 | 1.0637 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 | 0.646469 |

| 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 | 0.649558 |

| 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 | 0.652856 |

| 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 | 0.653490 |

| 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 | 0.658621 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 1.0905 | 160.46 | 1.9558 | 24.786 | 7.4568 | 0.85543 | 0.9415 | 0.679609 |

| 2024-01-23 | 1.0872 | 160.88 | 1.9558 | 24.824 | 7.4574 | 0.85493 | 0.9446 | 0.675783 |

| 2024-01-22 | 1.0890 | 160.95 | 1.9558 | 24.758 | 7.4585 | 0.85575 | 0.9458 | 0.676608 |

| 2024-01-19 | 1.0887 | 161.17 | 1.9558 | 24.813 | 7.4575 | 0.85825 | 0.9459 | 0.675498 |

| 2024-01-18 | 1.0875 | 160.89 | 1.9558 | 24.734 | 7.4571 | 0.85773 | 0.9432 | 0.675928 |

62 rows × 8 columns

df.head()| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | 1.0637 | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 |

| 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 |

| 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 |

| 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 |

| 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 |

Concatenating

new_col = 100 * df_copy.JPY/df_copy.USDpd.concat([df_copy['USD'], new_col]) # vertical stackingTime

2024-04-16 1.063700

2024-04-15 1.065600

2024-04-12 1.065200

2024-04-11 1.072900

2024-04-10 1.086000

...

2024-01-24 14714.351215

2024-01-23 14797.645327

2024-01-22 14779.614325

2024-01-19 14803.894553

2024-01-18 14794.482759

Length: 124, dtype: float64pd.concat([df_copy['USD'], new_col], axis=1) # horizontal stacking| USD | 0 | |

|---|---|---|

| Time | ||

| 2024-04-16 | 1.0637 | 15468.647175 |

| 2024-04-15 | 1.0656 | 15395.082583 |

| 2024-04-12 | 1.0652 | 15317.311303 |

| 2024-04-11 | 1.0729 | 15302.451300 |

| 2024-04-10 | 1.0860 | 15183.241252 |

| ... | ... | ... |

| 2024-01-24 | 1.0905 | 14714.351215 |

| 2024-01-23 | 1.0872 | 14797.645327 |

| 2024-01-22 | 1.0890 | 14779.614325 |

| 2024-01-19 | 1.0887 | 14803.894553 |

| 2024-01-18 | 1.0875 | 14794.482759 |

62 rows × 2 columns

Summary statistics

Pandas objects have a set of common mathematical and statistical methods. Most of these fall into the category of reductions or summary statistics, methods that extract a single value (like the sum or mean) from a Series, or a Series of values from the rows or columns of a DataFrame. Pandas methods have built-in handling for missing data (unlike NumPy methods). Specifically, the default for pandas methods is skipna=True, which excludes NA/null values when computing the result.

df.mean()USD 1.082711

JPY 162.195484

BGN 1.955800

CZK 25.199081

DKK 7.456484

GBP 0.855201

CHF 0.957208

dtype: float64df_na = df.copy()df_na.iloc[0, 0] = np.nandf_na.head()| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | NaN | 164.54 | 1.9558 | 25.210 | 7.4609 | 0.85440 | 0.9712 |

| 2024-04-15 | 1.0656 | 164.05 | 1.9558 | 25.324 | 7.4606 | 0.85405 | 0.9725 |

| 2024-04-12 | 1.0652 | 163.16 | 1.9558 | 25.337 | 7.4603 | 0.85424 | 0.9716 |

| 2024-04-11 | 1.0729 | 164.18 | 1.9558 | 25.392 | 7.4604 | 0.85525 | 0.9787 |

| 2024-04-10 | 1.0860 | 164.89 | 1.9558 | 25.368 | 7.4594 | 0.85515 | 0.9810 |

df_na.mean()USD 1.083023

JPY 162.195484

BGN 1.955800

CZK 25.199081

DKK 7.456484

GBP 0.855201

CHF 0.957208

dtype: float64df_na.mean(skipna=False)USD NaN

JPY 162.195484

BGN 1.955800

CZK 25.199081

DKK 7.456484

GBP 0.855201

CHF 0.957208

dtype: float64df.describe()| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| count | 62.000000 | 62.000000 | 6.200000e+01 | 62.000000 | 62.000000 | 62.000000 | 62.000000 |

| mean | 1.082711 | 162.195484 | 1.955800e+00 | 25.199081 | 7.456484 | 0.855201 | 0.957208 |

| std | 0.006755 | 1.623635 | 2.686287e-15 | 0.220672 | 0.002161 | 0.001680 | 0.015174 |

| min | 1.063700 | 158.960000 | 1.955800e+00 | 24.734000 | 7.453600 | 0.850980 | 0.931500 |

| 25% | 1.078550 | 160.905000 | 1.955800e+00 | 25.046000 | 7.454425 | 0.854267 | 0.944900 |

| 50% | 1.083900 | 162.150000 | 1.955800e+00 | 25.297000 | 7.456500 | 0.855125 | 0.956150 |

| 75% | 1.087350 | 163.432500 | 1.955800e+00 | 25.354000 | 7.458200 | 0.856272 | 0.971500 |

| max | 1.093900 | 164.970000 | 1.955800e+00 | 25.460000 | 7.460900 | 0.858460 | 0.984600 |

df.describe(percentiles=[0.01, 0.05, 0.25, 0.75, 0.95])| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| count | 62.000000 | 62.000000 | 6.200000e+01 | 62.000000 | 62.000000 | 62.000000 | 62.000000 |

| mean | 1.082711 | 162.195484 | 1.955800e+00 | 25.199081 | 7.456484 | 0.855201 | 0.957208 |

| std | 0.006755 | 1.623635 | 2.686287e-15 | 0.220672 | 0.002161 | 0.001680 | 0.015174 |

| min | 1.063700 | 158.960000 | 1.955800e+00 | 24.734000 | 7.453600 | 0.850980 | 0.931500 |

| 1% | 1.064615 | 159.326000 | 1.955800e+00 | 24.742540 | 7.453661 | 0.851407 | 0.932781 |

| 5% | 1.071380 | 159.710500 | 1.955800e+00 | 24.759400 | 7.453905 | 0.852504 | 0.934705 |

| 25% | 1.078550 | 160.905000 | 1.955800e+00 | 25.046000 | 7.454425 | 0.854267 | 0.944900 |

| 50% | 1.083900 | 162.150000 | 1.955800e+00 | 25.297000 | 7.456500 | 0.855125 | 0.956150 |

| 75% | 1.087350 | 163.432500 | 1.955800e+00 | 25.354000 | 7.458200 | 0.856272 | 0.971500 |

| 95% | 1.092455 | 164.682500 | 1.955800e+00 | 25.414800 | 7.460395 | 0.857946 | 0.981000 |

| max | 1.093900 | 164.970000 | 1.955800e+00 | 25.460000 | 7.460900 | 0.858460 | 0.984600 |

df[['USD', 'CHF', 'CZK']].describe()| USD | CHF | CZK | |

|---|---|---|---|

| count | 62.000000 | 62.000000 | 62.000000 |

| mean | 1.082711 | 0.957208 | 25.199081 |

| std | 0.006755 | 0.015174 | 0.220672 |

| min | 1.063700 | 0.931500 | 24.734000 |

| 25% | 1.078550 | 0.944900 | 25.046000 |

| 50% | 1.083900 | 0.956150 | 25.297000 |

| 75% | 1.087350 | 0.971500 | 25.354000 |

| max | 1.093900 | 0.984600 | 25.460000 |

df.mean() USD 1.082711

JPY 162.195484

BGN 1.955800

CZK 25.199081

DKK 7.456484

GBP 0.855201

CHF 0.957208

dtype: float64df.median()USD 1.083900

JPY 162.150000

BGN 1.955800

CZK 25.297000

DKK 7.456500

GBP 0.855125

CHF 0.956150

dtype: float64df.min()USD 1.06370

JPY 158.96000

BGN 1.95580

CZK 24.73400

DKK 7.45360

GBP 0.85098

CHF 0.93150

dtype: float64type(df.mean())pandas.core.series.Seriesdf.agg(['mean', 'median']) # aggregate multiple statistics together| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| mean | 1.082711 | 162.195484 | 1.9558 | 25.199081 | 7.456484 | 0.855201 | 0.957208 |

| median | 1.083900 | 162.150000 | 1.9558 | 25.297000 | 7.456500 | 0.855125 | 0.956150 |

Correlation

df['USD'].corr(df['JPY'])np.float64(-0.10333665136813898)df.corr()| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| USD | 1.000000 | -0.103337 | NaN | -0.218888 | -0.232007 | 0.074199 | -0.042449 |

| JPY | -0.103337 | 1.000000 | NaN | 0.655093 | 0.463510 | 0.484794 | 0.901636 |

| BGN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| CZK | -0.218888 | 0.655093 | NaN | 1.000000 | 0.008358 | 0.128065 | 0.649767 |

| DKK | -0.232007 | 0.463510 | NaN | 0.008358 | 1.000000 | 0.307508 | 0.604572 |

| GBP | 0.074199 | 0.484794 | NaN | 0.128065 | 0.307508 | 1.000000 | 0.424830 |

| CHF | -0.042449 | 0.901636 | NaN | 0.649767 | 0.604572 | 0.424830 | 1.000000 |

df.corrwith(df['USD'])USD 1.000000e+00

JPY -1.033367e-01

BGN -3.260316e-14

CZK -2.188876e-01

DKK -2.320074e-01

GBP 7.419901e-02

CHF -4.244863e-02

dtype: float64Operations between series

s1 = df['USD'].iloc[0:5].copy()

s1Time

2024-04-16 1.0637

2024-04-15 1.0656

2024-04-12 1.0652

2024-04-11 1.0729

2024-04-10 1.0860

Name: USD, dtype: float64s2 = df['USD'].iloc[2:7].copy()

s2Time

2024-04-12 1.0652

2024-04-11 1.0729

2024-04-10 1.0860

2024-04-09 1.0867

2024-04-08 1.0823

Name: USD, dtype: float64s1 + s2Time

2024-04-08 NaN

2024-04-09 NaN

2024-04-10 2.1720

2024-04-11 2.1458

2024-04-12 2.1304

2024-04-15 NaN

2024-04-16 NaN

Freq: B, Name: USD, dtype: float64df1 = df.iloc[0:4, 0:3].copy()

df1| USD | JPY | BGN | |

|---|---|---|---|

| Time | |||

| 2024-04-16 | 1.0637 | 164.54 | 1.9558 |

| 2024-04-15 | 1.0656 | 164.05 | 1.9558 |

| 2024-04-12 | 1.0652 | 163.16 | 1.9558 |

| 2024-04-11 | 1.0729 | 164.18 | 1.9558 |

df2 = df.iloc[1:5, 1:4].copy()

df2| JPY | BGN | CZK | |

|---|---|---|---|

| Time | |||

| 2024-04-15 | 164.05 | 1.9558 | 25.324 |

| 2024-04-12 | 163.16 | 1.9558 | 25.337 |

| 2024-04-11 | 164.18 | 1.9558 | 25.392 |

| 2024-04-10 | 164.89 | 1.9558 | 25.368 |

df1 + df2| BGN | CZK | JPY | USD | |

|---|---|---|---|---|

| Time | ||||

| 2024-04-10 | NaN | NaN | NaN | NaN |

| 2024-04-11 | 3.9116 | NaN | 328.36 | NaN |

| 2024-04-12 | 3.9116 | NaN | 326.32 | NaN |

| 2024-04-15 | 3.9116 | NaN | 328.10 | NaN |

| 2024-04-16 | NaN | NaN | NaN | NaN |

When one dataframe is a subset of the other, you can do the following.

df1| USD | JPY | BGN | |

|---|---|---|---|

| Time | |||

| 2024-04-16 | 1.0637 | 164.54 | 1.9558 |

| 2024-04-15 | 1.0656 | 164.05 | 1.9558 |

| 2024-04-12 | 1.0652 | 163.16 | 1.9558 |

| 2024-04-11 | 1.0729 | 164.18 | 1.9558 |

df3 = df.iloc[0:3, 0:2].copy()

df3| USD | JPY | |

|---|---|---|

| Time | ||

| 2024-04-16 | 1.0637 | 164.54 |

| 2024-04-15 | 1.0656 | 164.05 |

| 2024-04-12 | 1.0652 | 163.16 |

df1.add(df3, fill_value=0)| BGN | JPY | USD | |

|---|---|---|---|

| Time | |||

| 2024-04-11 | 1.9558 | 164.18 | 1.0729 |

| 2024-04-12 | 1.9558 | 326.32 | 2.1304 |

| 2024-04-15 | 1.9558 | 328.10 | 2.1312 |

| 2024-04-16 | 1.9558 | 329.08 | 2.1274 |

Operations between dataframes and series

Operations between a dataframe and series follow similar broadcasting rules to numpy.

arr = np.arange(12.).reshape((3, 4))print(arr.shape, arr[0].shape) # trailing dimensions match(3, 4) (4,)arrarray([[ 0., 1., 2., 3.],

[ 4., 5., 6., 7.],

[ 8., 9., 10., 11.]])arr - arr[0]array([[0., 0., 0., 0.],

[4., 4., 4., 4.],

[8., 8., 8., 8.]])frame = pd.DataFrame(np.arange(12.).reshape((4, 3)), columns=list("bde"), index=["Utah", "Ohio", "Texas", "Oregon"])

series = frame.iloc[0]frame - series| b | d | e | |

|---|---|---|---|

| Utah | 0.0 | 0.0 | 0.0 |

| Ohio | 3.0 | 3.0 | 3.0 |

| Texas | 6.0 | 6.0 | 6.0 |

| Oregon | 9.0 | 9.0 | 9.0 |

series2 = pd.Series(np.arange(3), index=["b", "e", "f"])

frame + series2| b | d | e | f | |

|---|---|---|---|---|

| Utah | 0.0 | NaN | 3.0 | NaN |

| Ohio | 3.0 | NaN | 6.0 | NaN |

| Texas | 6.0 | NaN | 9.0 | NaN |

| Oregon | 9.0 | NaN | 12.0 | NaN |

If you want to instead broadcast over the columns, matching on the rows, you have to use one of the arithmetic methods and specify to match over the index. For example:

series3 = frame["d"]

series3Utah 1.0

Ohio 4.0

Texas 7.0

Oregon 10.0

Name: d, dtype: float64frame.sub(series3, axis="index")| b | d | e | |

|---|---|---|---|

| Utah | -1.0 | 0.0 | 1.0 |

| Ohio | -1.0 | 0.0 | 1.0 |

| Texas | -1.0 | 0.0 | 1.0 |

| Oregon | -1.0 | 0.0 | 1.0 |

frame.sub(series3) # this doesn't do the right thing| Ohio | Oregon | Texas | Utah | b | d | e | |

|---|---|---|---|---|---|---|---|

| Utah | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| Ohio | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| Texas | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| Oregon | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

Standardizing dataframes

df.mean()USD 1.082711

JPY 162.195484

BGN 1.955800

CZK 25.199081

DKK 7.456484

GBP 0.855201

CHF 0.957208

dtype: float64df - df.mean()| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | -0.019011 | 2.344516 | 4.440892e-16 | 0.010919 | 0.004416 | -0.000801 | 0.013992 |

| 2024-04-15 | -0.017111 | 1.854516 | 4.440892e-16 | 0.124919 | 0.004116 | -0.001151 | 0.015292 |

| 2024-04-12 | -0.017511 | 0.964516 | 4.440892e-16 | 0.137919 | 0.003816 | -0.000961 | 0.014392 |

| 2024-04-11 | -0.009811 | 1.984516 | 4.440892e-16 | 0.192919 | 0.003916 | 0.000049 | 0.021492 |

| 2024-04-10 | 0.003289 | 2.694516 | 4.440892e-16 | 0.168919 | 0.002916 | -0.000051 | 0.023792 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 0.007789 | -1.735484 | 4.440892e-16 | -0.413081 | 0.000316 | 0.000229 | -0.015708 |

| 2024-01-23 | 0.004489 | -1.315484 | 4.440892e-16 | -0.375081 | 0.000916 | -0.000271 | -0.012608 |

| 2024-01-22 | 0.006289 | -1.245484 | 4.440892e-16 | -0.441081 | 0.002016 | 0.000549 | -0.011408 |

| 2024-01-19 | 0.005989 | -1.025484 | 4.440892e-16 | -0.386081 | 0.001016 | 0.003049 | -0.011308 |

| 2024-01-18 | 0.004789 | -1.305484 | 4.440892e-16 | -0.465081 | 0.000616 | 0.002529 | -0.014008 |

62 rows × 7 columns

df.sub(df.mean())| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | -0.019011 | 2.344516 | 4.440892e-16 | 0.010919 | 0.004416 | -0.000801 | 0.013992 |

| 2024-04-15 | -0.017111 | 1.854516 | 4.440892e-16 | 0.124919 | 0.004116 | -0.001151 | 0.015292 |

| 2024-04-12 | -0.017511 | 0.964516 | 4.440892e-16 | 0.137919 | 0.003816 | -0.000961 | 0.014392 |

| 2024-04-11 | -0.009811 | 1.984516 | 4.440892e-16 | 0.192919 | 0.003916 | 0.000049 | 0.021492 |

| 2024-04-10 | 0.003289 | 2.694516 | 4.440892e-16 | 0.168919 | 0.002916 | -0.000051 | 0.023792 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 0.007789 | -1.735484 | 4.440892e-16 | -0.413081 | 0.000316 | 0.000229 | -0.015708 |

| 2024-01-23 | 0.004489 | -1.315484 | 4.440892e-16 | -0.375081 | 0.000916 | -0.000271 | -0.012608 |

| 2024-01-22 | 0.006289 | -1.245484 | 4.440892e-16 | -0.441081 | 0.002016 | 0.000549 | -0.011408 |

| 2024-01-19 | 0.005989 | -1.025484 | 4.440892e-16 | -0.386081 | 0.001016 | 0.003049 | -0.011308 |

| 2024-01-18 | 0.004789 | -1.305484 | 4.440892e-16 | -0.465081 | 0.000616 | 0.002529 | -0.014008 |

62 rows × 7 columns

df.sub(df.mean()).mean() # almost zero: successUSD -2.184632e-16

JPY 3.483951e-14

BGN 4.440892e-16

CZK -5.042561e-15

DKK -9.311548e-16

GBP 1.146037e-16

CHF -2.148819e-17

dtype: float64df.sub(df.mean(), axis="columns")| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | -0.019011 | 2.344516 | 4.440892e-16 | 0.010919 | 0.004416 | -0.000801 | 0.013992 |

| 2024-04-15 | -0.017111 | 1.854516 | 4.440892e-16 | 0.124919 | 0.004116 | -0.001151 | 0.015292 |

| 2024-04-12 | -0.017511 | 0.964516 | 4.440892e-16 | 0.137919 | 0.003816 | -0.000961 | 0.014392 |

| 2024-04-11 | -0.009811 | 1.984516 | 4.440892e-16 | 0.192919 | 0.003916 | 0.000049 | 0.021492 |

| 2024-04-10 | 0.003289 | 2.694516 | 4.440892e-16 | 0.168919 | 0.002916 | -0.000051 | 0.023792 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 0.007789 | -1.735484 | 4.440892e-16 | -0.413081 | 0.000316 | 0.000229 | -0.015708 |

| 2024-01-23 | 0.004489 | -1.315484 | 4.440892e-16 | -0.375081 | 0.000916 | -0.000271 | -0.012608 |

| 2024-01-22 | 0.006289 | -1.245484 | 4.440892e-16 | -0.441081 | 0.002016 | 0.000549 | -0.011408 |

| 2024-01-19 | 0.005989 | -1.025484 | 4.440892e-16 | -0.386081 | 0.001016 | 0.003049 | -0.011308 |

| 2024-01-18 | 0.004789 | -1.305484 | 4.440892e-16 | -0.465081 | 0.000616 | 0.002529 | -0.014008 |

62 rows × 7 columns

# also works, but maybe less explicit than axis="columns"

df.sub(df.mean(), axis=1).mean()USD -2.184632e-16

JPY 3.483951e-14

BGN 4.440892e-16

CZK -5.042561e-15

DKK -9.311548e-16

GBP 1.146037e-16

CHF -2.148819e-17

dtype: float64df_standardized = (df-df.mean())/df.std()df_standardized2 = df.sub(df.mean()).div(df.std())# most explicit

df_standardized3 = df.sub(df.mean(), axis="columns").div(df.std(), axis="columns")df_standardized4 = df.sub(df.mean(), axis=1).div(df.std(), axis=1)((df_standardized4-df_standardized) == 0.).all()USD True

JPY True

BGN True

CZK True

DKK True

GBP True

CHF True

dtype: booldf_max_standardized = df/df.max()df_standardized| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | -2.814246 | 1.443993 | 0.165317 | 0.049482 | 2.043993 | -0.476651 | 0.922100 |

| 2024-04-15 | -2.532988 | 1.142200 | 0.165317 | 0.566086 | 1.905139 | -0.684975 | 1.007773 |

| 2024-04-12 | -2.592200 | 0.594048 | 0.165317 | 0.624997 | 1.766285 | -0.571885 | 0.948461 |

| 2024-04-11 | -1.452368 | 1.222268 | 0.165317 | 0.874235 | 1.812570 | 0.029281 | 1.416367 |

| 2024-04-10 | 0.486828 | 1.659558 | 0.165317 | 0.765476 | 1.349722 | -0.030241 | 1.567942 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 1.152964 | -1.068888 | 0.165317 | -1.871920 | 0.146319 | 0.136419 | -1.035197 |

| 2024-01-23 | 0.664465 | -0.810209 | 0.165317 | -1.699719 | 0.424028 | -0.161188 | -0.830900 |

| 2024-01-22 | 0.930919 | -0.767096 | 0.165317 | -1.998805 | 0.933160 | 0.326887 | -0.751817 |

| 2024-01-19 | 0.886510 | -0.631598 | 0.165317 | -1.749567 | 0.470313 | 1.814921 | -0.745227 |

| 2024-01-18 | 0.708874 | -0.804050 | 0.165317 | -2.107564 | 0.285174 | 1.505410 | -0.923163 |

62 rows × 7 columns

Function application and mapping

def f1(x):

return x.max() - x.min()df.apply(f1) # applies across rows by defaultUSD 0.03020

JPY 6.01000

BGN 0.00000

CZK 0.72600

DKK 0.00730

GBP 0.00748

CHF 0.05310

dtype: float64df.apply(f1, axis='columns')Time

2024-04-16 163.68560

2024-04-15 163.19595

2024-04-12 162.30576

2024-04-11 163.32475

2024-04-10 164.03485

...

2024-01-24 159.60457

2024-01-23 160.02507

2024-01-22 160.09425

2024-01-19 160.31175

2024-01-18 160.03227

Length: 62, dtype: float64def f2(x):

return pd.Series([x.min(), x.max()], index=["min", "max"])df.apply(f2)| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| min | 1.0637 | 158.96 | 1.9558 | 24.734 | 7.4536 | 0.85098 | 0.9315 |

| max | 1.0939 | 164.97 | 1.9558 | 25.460 | 7.4609 | 0.85846 | 0.9846 |

def my_format(x):

return f"{x:.2f}"For element-wise operations, use pd.DataFrame.map:

df.map(my_format) | USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | 1.06 | 164.54 | 1.96 | 25.21 | 7.46 | 0.85 | 0.97 |

| 2024-04-15 | 1.07 | 164.05 | 1.96 | 25.32 | 7.46 | 0.85 | 0.97 |

| 2024-04-12 | 1.07 | 163.16 | 1.96 | 25.34 | 7.46 | 0.85 | 0.97 |

| 2024-04-11 | 1.07 | 164.18 | 1.96 | 25.39 | 7.46 | 0.86 | 0.98 |

| 2024-04-10 | 1.09 | 164.89 | 1.96 | 25.37 | 7.46 | 0.86 | 0.98 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 1.09 | 160.46 | 1.96 | 24.79 | 7.46 | 0.86 | 0.94 |

| 2024-01-23 | 1.09 | 160.88 | 1.96 | 24.82 | 7.46 | 0.85 | 0.94 |

| 2024-01-22 | 1.09 | 160.95 | 1.96 | 24.76 | 7.46 | 0.86 | 0.95 |

| 2024-01-19 | 1.09 | 161.17 | 1.96 | 24.81 | 7.46 | 0.86 | 0.95 |

| 2024-01-18 | 1.09 | 160.89 | 1.96 | 24.73 | 7.46 | 0.86 | 0.94 |

62 rows × 7 columns

df.map(lambda x: f"{x:.2f}")| USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|

| Time | |||||||

| 2024-04-16 | 1.06 | 164.54 | 1.96 | 25.21 | 7.46 | 0.85 | 0.97 |

| 2024-04-15 | 1.07 | 164.05 | 1.96 | 25.32 | 7.46 | 0.85 | 0.97 |

| 2024-04-12 | 1.07 | 163.16 | 1.96 | 25.34 | 7.46 | 0.85 | 0.97 |

| 2024-04-11 | 1.07 | 164.18 | 1.96 | 25.39 | 7.46 | 0.86 | 0.98 |

| 2024-04-10 | 1.09 | 164.89 | 1.96 | 25.37 | 7.46 | 0.86 | 0.98 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-01-24 | 1.09 | 160.46 | 1.96 | 24.79 | 7.46 | 0.86 | 0.94 |

| 2024-01-23 | 1.09 | 160.88 | 1.96 | 24.82 | 7.46 | 0.85 | 0.94 |

| 2024-01-22 | 1.09 | 160.95 | 1.96 | 24.76 | 7.46 | 0.86 | 0.95 |

| 2024-01-19 | 1.09 | 161.17 | 1.96 | 24.81 | 7.46 | 0.86 | 0.95 |

| 2024-01-18 | 1.09 | 160.89 | 1.96 | 24.73 | 7.46 | 0.86 | 0.94 |

62 rows × 7 columns

Wide vs. long data formats

df_standardized = df_standardized.reset_index() # turn time back into a columndf_standardized.head()| Time | USD | JPY | BGN | CZK | DKK | GBP | CHF | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2024-04-16 | -2.814246 | 1.443993 | 0.165317 | 0.049482 | 2.043993 | -0.476651 | 0.922100 |

| 1 | 2024-04-15 | -2.532988 | 1.142200 | 0.165317 | 0.566086 | 1.905139 | -0.684975 | 1.007773 |

| 2 | 2024-04-12 | -2.592200 | 0.594048 | 0.165317 | 0.624997 | 1.766285 | -0.571885 | 0.948461 |

| 3 | 2024-04-11 | -1.452368 | 1.222268 | 0.165317 | 0.874235 | 1.812570 | 0.029281 | 1.416367 |

| 4 | 2024-04-10 | 0.486828 | 1.659558 | 0.165317 | 0.765476 | 1.349722 | -0.030241 | 1.567942 |

The data is in what’s known as a ‘wide’ format. This is because the currency is in each of the columns. We can transform it to a ‘long’ format by using melt with arguments:

id_vars: this is the column to be used as identifier variablesvar_name: this is the new column which will contain the names of the columns in wide formatvalue_name: this is the new column which will contain the values of the columns in wide format

df_long = df_standardized.melt(id_vars='Time', var_name='currency', value_name='rate')df_long| Time | currency | rate | |

|---|---|---|---|

| 0 | 2024-04-16 | USD | -2.814246 |

| 1 | 2024-04-15 | USD | -2.532988 |

| 2 | 2024-04-12 | USD | -2.592200 |

| 3 | 2024-04-11 | USD | -1.452368 |

| 4 | 2024-04-10 | USD | 0.486828 |

| ... | ... | ... | ... |

| 429 | 2024-01-24 | CHF | -1.035197 |

| 430 | 2024-01-23 | CHF | -0.830900 |

| 431 | 2024-01-22 | CHF | -0.751817 |

| 432 | 2024-01-19 | CHF | -0.745227 |

| 433 | 2024-01-18 | CHF | -0.923163 |

434 rows × 3 columns

This “long’ format is an example of a”tidy data frame”, which we will discuss in more detail next lecture.

To go back to the “wide” format, we can use the pivot method:

df_long.pivot(index=['Time'], # column which will be the index

columns=['currency'], # variable which will expand out to columns

values=['rate']) # values in the table| rate | |||||||

|---|---|---|---|---|---|---|---|

| currency | BGN | CHF | CZK | DKK | GBP | JPY | USD |

| Time | |||||||

| 2024-01-18 | 0.165317 | -0.923163 | -2.107564 | 0.285174 | 1.505410 | -0.804050 | 0.708874 |

| 2024-01-19 | 0.165317 | -0.745227 | -1.749567 | 0.470313 | 1.814921 | -0.631598 | 0.886510 |

| 2024-01-22 | 0.165317 | -0.751817 | -1.998805 | 0.933160 | 0.326887 | -0.767096 | 0.930919 |

| 2024-01-23 | 0.165317 | -0.830900 | -1.699719 | 0.424028 | -0.161188 | -0.810209 | 0.664465 |

| 2024-01-24 | 0.165317 | -1.035197 | -1.871920 | 0.146319 | 0.136419 | -1.068888 | 1.152964 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-04-10 | 0.165317 | 1.567942 | 0.765476 | 1.349722 | -0.030241 | 1.659558 | 0.486828 |

| 2024-04-11 | 0.165317 | 1.416367 | 0.874235 | 1.812570 | 0.029281 | 1.222268 | -1.452368 |

| 2024-04-12 | 0.165317 | 0.948461 | 0.624997 | 1.766285 | -0.571885 | 0.594048 | -2.592200 |

| 2024-04-15 | 0.165317 | 1.007773 | 0.566086 | 1.905139 | -0.684975 | 1.142200 | -2.532988 |

| 2024-04-16 | 0.165317 | 0.922100 | 0.049482 | 2.043993 | -0.476651 | 1.443993 | -2.814246 |

62 rows × 7 columns

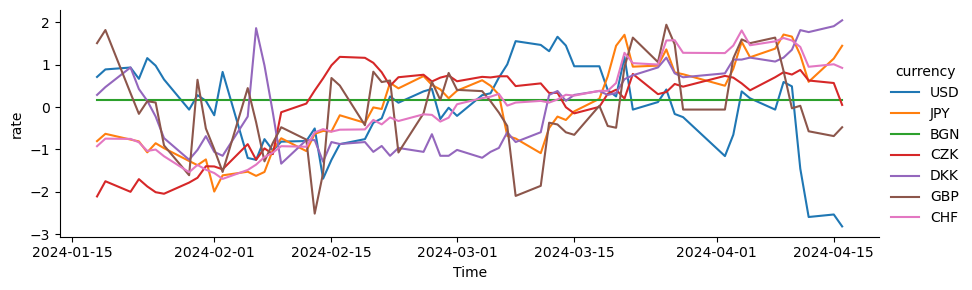

Example visualization with seaborn

We use the “long” data for a Seaborn plot:

sns.relplot(data=df_long,

x='Time',

y='rate',

hue='currency',

kind='line',

height=3,

aspect=3)