import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

from numpy.linalg import solve

np.random.seed(1)

import warnings

warnings.filterwarnings('ignore')Lecture 3 - Linear Regression

Linear Regression

Housing Dataset

We consider the Kings County housing dataset. It includes homes sold between May 2014 and May 2015.

Specifically, we focuse on the Rainier Valley zipcode.

# Load the dataset

house = pd.read_csv("data/rainier_valley_house.csv")house.columnsIndex(['Unnamed: 0', 'id', 'date', 'price', 'bedrooms', 'bathrooms',

'sqft_living', 'sqft_lot', 'floors', 'waterfront', 'view', 'condition',

'grade', 'sqft_above', 'sqft_basement', 'yr_built', 'yr_renovated',

'zipcode', 'lat', 'long', 'sqft_living15', 'sqft_lot15'],

dtype='object')# We will consider this subset of features

features = ["floors", "grade", "condition", "view", "sqft_living",

"sqft_lot", "sqft_basement", "yr_built", "yr_renovated",

"bedrooms", "bathrooms", "lat", "long"]

house = house[house['price'] < 1e6]

Y = house['price'] / 1000

X = house[features]

## Standardize the features

scaler = StandardScaler()

X_stan = scaler.fit_transform(X)Linear Regression Formula

We compute the regression coefficients using the formula:

\widehat{\beta} = (X^\top X)^{-1}X^\top y

## linear regression

X_stan1 = np.hstack([np.ones((X_stan.shape[0], 1)), X_stan])

X_train, X_test, Y_train, Y_test = train_test_split(X_stan1, Y, test_size=100, train_size=400, random_state=2)

betahat = np.linalg.inv(X_train.T @ X_train) @ (X_train.T @ Y_train)

Y_pred = X_test @ betahat

test_error = np.sqrt(((Y_test - Y_pred) ** 2).mean())

baseline_error = np.sqrt(((Y_test - Y_train.mean()) ** 2).mean())

## print coefficients

print("Coefficients:")

features_list = ['Intercept'] + list(X.columns)

for i, f in enumerate(features_list):

print(f"{f}: {betahat[i]:.3f}")

print(f"Test RMSE of linear regression: {test_error:.3f} Baseline RMSE: {baseline_error:.3f}")

R2 = 1 - test_error**2 / baseline_error**2

print(f"Test R-squared of linear regression: {R2:.3f}")Coefficients:

Intercept: 397.667

floors: 7.706

grade: 44.060

condition: 17.140

view: 27.275

sqft_living: 72.711

sqft_lot: 12.589

sqft_basement: -12.538

yr_built: -13.716

yr_renovated: 2.193

bedrooms: -19.933

bathrooms: 10.003

lat: 70.999

long: 29.816

Test RMSE of linear regression: 84.774 Baseline RMSE: 151.875

Test R-squared of linear regression: 0.688Using statsmodels

We can also use statsmodels to run linear regression for us:

import statsmodels.api as sm

model = sm.OLS(Y_train, X_train)

results = model.fit()results.paramsconst 397.666919

x1 7.705884

x2 44.059690

x3 17.140391

x4 27.274524

x5 72.711224

x6 12.589442

x7 -12.538127

x8 -13.716293

x9 2.192980

x10 -19.933029

x11 10.002684

x12 70.999486

x13 29.815873

dtype: float64coeffs = results.paramsY_pred = results.get_prediction(X_test)

Y_pred = Y_pred.predicted_mean

test_error = np.sqrt(((Y_test - Y_pred) ** 2).mean())

baseline_error = np.sqrt(((Y_test - Y_train.mean()) ** 2).mean())

print(f"Test RMSE of linear regression: {test_error:.3f} Baseline RMSE: {baseline_error:.3f}")

R2 = 1 - test_error**2 / baseline_error**2

print(f"Test R-squared of linear regression: {R2:.3f}")Test RMSE of linear regression: 84.774 Baseline RMSE: 151.875

Test R-squared of linear regression: 0.688Inference

t-tests for coefficients

results.summary()| Dep. Variable: | price | R-squared: | 0.729 |

| Model: | OLS | Adj. R-squared: | 0.720 |

| Method: | Least Squares | F-statistic: | 79.91 |

| Date: | Mon, 02 Mar 2026 | Prob (F-statistic): | 8.70e-101 |

| Time: | 16:16:27 | Log-Likelihood: | -2349.3 |

| No. Observations: | 400 | AIC: | 4727. |

| Df Residuals: | 386 | BIC: | 4783. |

| Df Model: | 13 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

| const | 397.6669 | 4.393 | 90.528 | 0.000 | 389.030 | 406.304 |

| x1 | 7.7059 | 6.882 | 1.120 | 0.264 | -5.826 | 21.238 |

| x2 | 44.0597 | 7.045 | 6.254 | 0.000 | 30.209 | 57.911 |

| x3 | 17.1404 | 4.790 | 3.579 | 0.000 | 7.723 | 26.557 |

| x4 | 27.2745 | 4.999 | 5.456 | 0.000 | 17.446 | 37.103 |

| x5 | 72.7112 | 10.910 | 6.665 | 0.000 | 51.261 | 94.161 |

| x6 | 12.5894 | 5.318 | 2.367 | 0.018 | 2.133 | 23.046 |

| x7 | -12.5381 | 7.710 | -1.626 | 0.105 | -27.696 | 2.620 |

| x8 | -13.7163 | 6.625 | -2.070 | 0.039 | -26.742 | -0.690 |

| x9 | 2.1930 | 4.533 | 0.484 | 0.629 | -6.720 | 11.106 |

| x10 | -19.9330 | 6.492 | -3.071 | 0.002 | -32.697 | -7.169 |

| x11 | 10.0027 | 8.088 | 1.237 | 0.217 | -5.899 | 25.904 |

| x12 | 70.9995 | 5.221 | 13.599 | 0.000 | 60.735 | 81.264 |

| x13 | 29.8159 | 5.281 | 5.646 | 0.000 | 19.434 | 40.198 |

| Omnibus: | 26.158 | Durbin-Watson: | 1.973 |

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 65.389 |

| Skew: | 0.285 | Prob(JB): | 6.32e-15 |

| Kurtosis: | 4.897 | Cond. No. | 6.12 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

# Extract confidence intervals from the summary table

conf_int = results.conf_int()Using the bootstrap

Y_train = Y_train.to_numpy()

n_train = X_train.shape[0]

beta = coeffs

n_boot = 1000

bootstrap_inds = [np.random.choice(range(1, n_train), n_train, replace=True) for _ in range(n_boot)]

boot_bhats = np.zeros((n_boot, X_train.shape[1]))

for b in range(n_boot):

X_boot = X_train[bootstrap_inds[b]]

Y_boot = Y_train[bootstrap_inds[b]]

linreg = sm.OLS(Y_boot, X_boot)

boot_result = linreg.fit()

boot_bhats[b, :] = boot_result.params

bins_beta = np.linspace(boot_bhats[:, 4].min(), boot_bhats[:, 4].max(), 20)

plt.figure(figsize=(4,3))

plt.hist(boot_bhats[:, 4], bins=bins_beta, alpha=0.7, color='green', label='Bootstrap Beta')

plt.title('Histogram of Bootstrap Betas')

plt.xlabel('Beta')

plt.ylabel('Frequency')

plt.legend()

beta_sds = np.std(boot_bhats, axis=0)# confidence interval

lower_quantiles = beta - 2 * beta_sds

upper_quantiles = beta + 2 * beta_sds

# Print results

print("95% Bootstrap Confidence Intervals for Coefficients:")

for i, f in enumerate(features_list):

print(f"{f}: ({lower_quantiles[i]:.3f}, {upper_quantiles[i]:.3f})")95% Bootstrap Confidence Intervals for Coefficients:

Intercept: (388.878, 406.456)

floors: (-6.717, 22.129)

grade: (27.224, 60.895)

condition: (7.662, 26.619)

view: (17.276, 37.273)

sqft_living: (48.540, 96.882)

sqft_lot: (-1.782, 26.961)

sqft_basement: (-29.503, 4.427)

yr_built: (-29.000, 1.567)

yr_renovated: (-7.993, 12.379)

bedrooms: (-35.586, -4.280)

bathrooms: (-7.101, 27.106)

lat: (60.028, 81.971)

long: (19.281, 40.350)Overfitting

Example with n=p

## Simulate data from linear model

p = 30

n_train = 30

n_test = 100

n = n_train + n_test

beta_true = 1/np.sqrt(p) * np.ones(p)

X = np.random.normal(size=(n, p))

noise = 0.5 * np.random.normal(size=(n))

Y = X @ beta_true + noise

X_train = X[:n_train, :]

Y_train = Y[:n_train]

X_test = X[n_train:, :]

Y_test = Y[n_train:]

betahat = np.linalg.solve(X_train.T @ X_train, X_train.T @ Y_train)

## print training error

train_error = np.mean((Y_train - X_train @ betahat)**2)

print(f"Training error: {train_error:.2f}")

## print test error

test_error = np.mean((Y_test - X_test @ betahat)**2)

print(f"Test error: {test_error:.2f}")Training error: 0.00

Test error: 8.11Example with polynomials

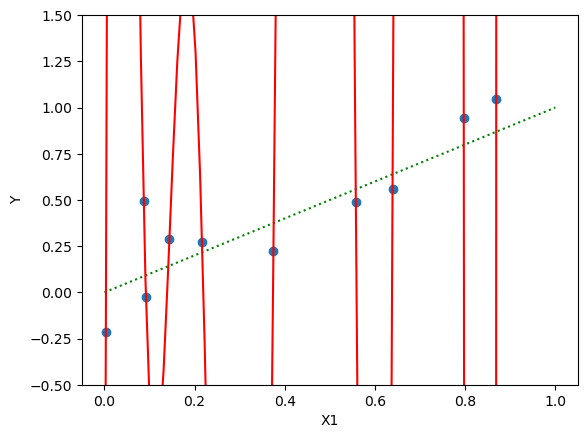

n = 10

X1 = np.random.uniform(size=(n))

noise = 0.2 * np.random.normal(size=(n))

Y = X1 + noise

## add polynomial of X1

p = 10

X = np.column_stack([X1**i for i in range(0, p+1)])

## fit linear model

betahat = np.linalg.solve(X.T @ X, X.T @ Y)

err = np.sum((Y - X @ betahat)**2)

print(f"Training error: {err:.2f}")

# plot X1, Y

import matplotlib.pyplot as plt

plt.scatter(X1, Y)

plt.xlabel('X1')

plt.ylabel('Y')

X1_grid = np.linspace(0, 1, 100)

# plot truth as dotted

Y_grid = X1_grid

plt.plot(X1_grid, Y_grid, color='green', linestyle='dotted')

# plot fitted curve

X_grid = np.column_stack([X1_grid**i for i in range(0, p+1)])

Y_grid = X_grid @ betahat

plt.ylim(-.5, 1.5)

plt.plot(X1_grid, Y_grid, color='red')

plt.show()Training error: 0.01

Some coefficients are very large:

-np.sort(-betahat) # np.sort is smallest to largest - use negative for largest to smallestarray([ 2.75524984e+07, 7.25216625e+06, 3.51473556e+06, 3.01842642e+05,

1.01149788e+03, -2.54649723e+00, -2.80791410e+04, -7.56886527e+05,

-1.53581036e+06, -1.31515994e+07, -2.31322672e+07])Linear Regression with Ridge Regularization

Ridge regularization shrinks coefficients \beta. The formula is:

\widehat{\beta} = (X^\top X + \lambda \bm{I})^{-1}X^\top y

We now consider a movies dataset where we want to predict revenue from the genre and other features.

# Load the dataset

movies = pd.read_csv("data/movies.csv")

## permute rows

np.random.seed(1)

movies = movies.sample(frac=1).reset_index(drop=True)

## remove rows with 0 revenue

movies = movies[movies['revenue'] > 0]

movies = movies.dropna()

# List of features

features = ["Action", "Crime", "Comedy",

"Adventure", "Drama", "Fantasy", "Music", "Western",

"Science Fiction", "Mystery", "Family", "Horror", "Romance",

"runtime", "budget"]

# Target variable

Y = movies['revenue']/1000000

X = movies[features]

# add interaction between first 10 features and budget

# for feature in features[:10]:

# X[feature + ':budget'] = X[feature] * X['budget']

# features = X.columns

print(f"Number of features: {X.shape[1]}")

# Split the data into test, learning (further divided into train and validation), and training sets

n_learn = 600

n_test = 300

Y_test = Y.iloc[:n_test]

Y_learn = Y.iloc[n_test:n_test+n_learn]

X_test = X.iloc[:n_test, :]

X_learn = X.iloc[n_test:n_test+n_learn, :]

stan_features = ["runtime", "budget"]

stan_mean = X_learn[stan_features].mean(axis=0)

stan_sd = X_learn[stan_features].std(axis=0)

X_stan = X_learn

X_stan[stan_features] = (X_learn[stan_features] - stan_mean) / stan_sd

# Add a column of ones to include the intercept in the model

X_stan = np.hstack([np.ones((X_stan.shape[0], 1)), X_stan])

# Candidate set for lambda

candidate_set = np.concatenate([[0], 2 ** np.arange(-5, 10, .5)])

K = 10

indices = np.arange(n_learn)

folds = indices.reshape(K, -1)

validerr = np.zeros((K, len(candidate_set)))

for k in range(K):

valid_ix = folds[k, :]

train_ix = np.delete(indices, folds[k, :])

X_valid = X_stan[valid_ix, :]

Y_valid = Y_learn.iloc[valid_ix]

X_train = X_stan[train_ix, :]

Y_train = Y_learn.iloc[train_ix]

for j, lambda_val in enumerate(candidate_set):

beta_lambda = solve(X_train.T @ X_train + lambda_val * np.eye(X_train.shape[1]),

X_train.T @ Y_train)

Y_lambda = X_valid @ beta_lambda

validerr[k, j] = np.sqrt(np.mean((Y_valid - Y_lambda) ** 2))

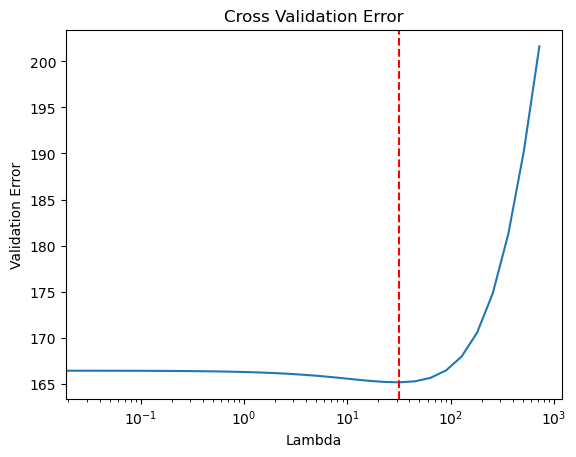

mean_valid_errs = validerr.mean(axis=0)

min_ix = np.argmin(mean_valid_errs)

lambda_best = candidate_set[min_ix]

beta_best = solve(X_stan.T @ X_stan + lambda_best * np.eye(X_stan.shape[1]),

X_stan.T @ Y_learn)

X_test_stan = X_test

X_test_stan[stan_features] = (X_test_stan[stan_features] - stan_mean)/stan_sd

X_test_stan = np.hstack([np.ones((X_test_stan.shape[0], 1)), X_test_stan])

Y_pred = X_test_stan @ beta_best

Y_baseline = Y_learn.mean()

## print coefficients

print("Coefficients: ")

print(f"Intercept: {beta_best[0]:.2f}")

for i in range(len(features)):

print(f"{features[i]}: {beta_best[i+1]:.2f}")

# Evaluate test error

test_error = np.sqrt(np.mean((Y_test - Y_pred) ** 2))

baseline_error = np.sqrt(np.mean((Y_test - Y_baseline) ** 2))

## print errors and R^2 with 2 sig figs

print("Test Error: {:.2f}".format(test_error))

print("Baseline Error: {:.2f}".format(baseline_error))

print("Test R-squared: {:.2f}".format(1 - test_error ** 2 / baseline_error ** 2))

Number of features: 15

Coefficients:

Intercept: 141.06

Action: -2.19

Crime: -9.17

Comedy: 7.34

Adventure: 60.97

Drama: -14.00

Fantasy: 30.55

Music: 0.94

Western: -6.38

Science Fiction: 38.08

Mystery: 4.88

Family: 41.90

Horror: 25.08

Romance: 7.92

runtime: 40.96

budget: 136.16

Test Error: 163.78

Baseline Error: 260.98

Test R-squared: 0.61## plot cross validation errors

import matplotlib.pyplot as plt

plt.plot(candidate_set, mean_valid_errs)

plt.axvline(x=lambda_best, color='r', linestyle='--')

plt.xlabel("Lambda")

plt.ylabel("Validation Error")

plt.title("Cross Validation Error")

plt.xscale('log')

plt.show()